India’s Employee Engagement Crisis Is Real — and Getting Worse Gallup’s State of the Global Workplace 2026 report delivers a sobering number on employee engagement: only 23% of Indian employees say they feel engaged at work. That is a sharp fall from 30% just a…

Category: Statutory Compliance

Statutory compliance guides from TMS – EPF, ESIC, Professional Tax, LWF, the new labour codes and HR compliance checklists for Indian employers.

-

Mid-Year HR Compliance Checklist 2026: 10 Things to Audit Before September

Why a Mid-Year Compliance Check Is Non-Negotiable in 2026 This HR compliance checklist covers what Indian employers must address now. The compliance landscape changed significantly in the past eight months. The four Labour Codes are now fully operational, the DPDP Act Rules are in effect,…

-

DPDP Act 2026: How to Handle Employee Data Without Getting Fined ₹250 Crore

The DPDP Act Is No Longer “Coming Soon” The Digital Personal Data Protection Act, 2023 is India’s first comprehensive data privacy law. With the Rules notified on 14 November 2025, the law is now fully operational — and it applies to every piece of digital…

-

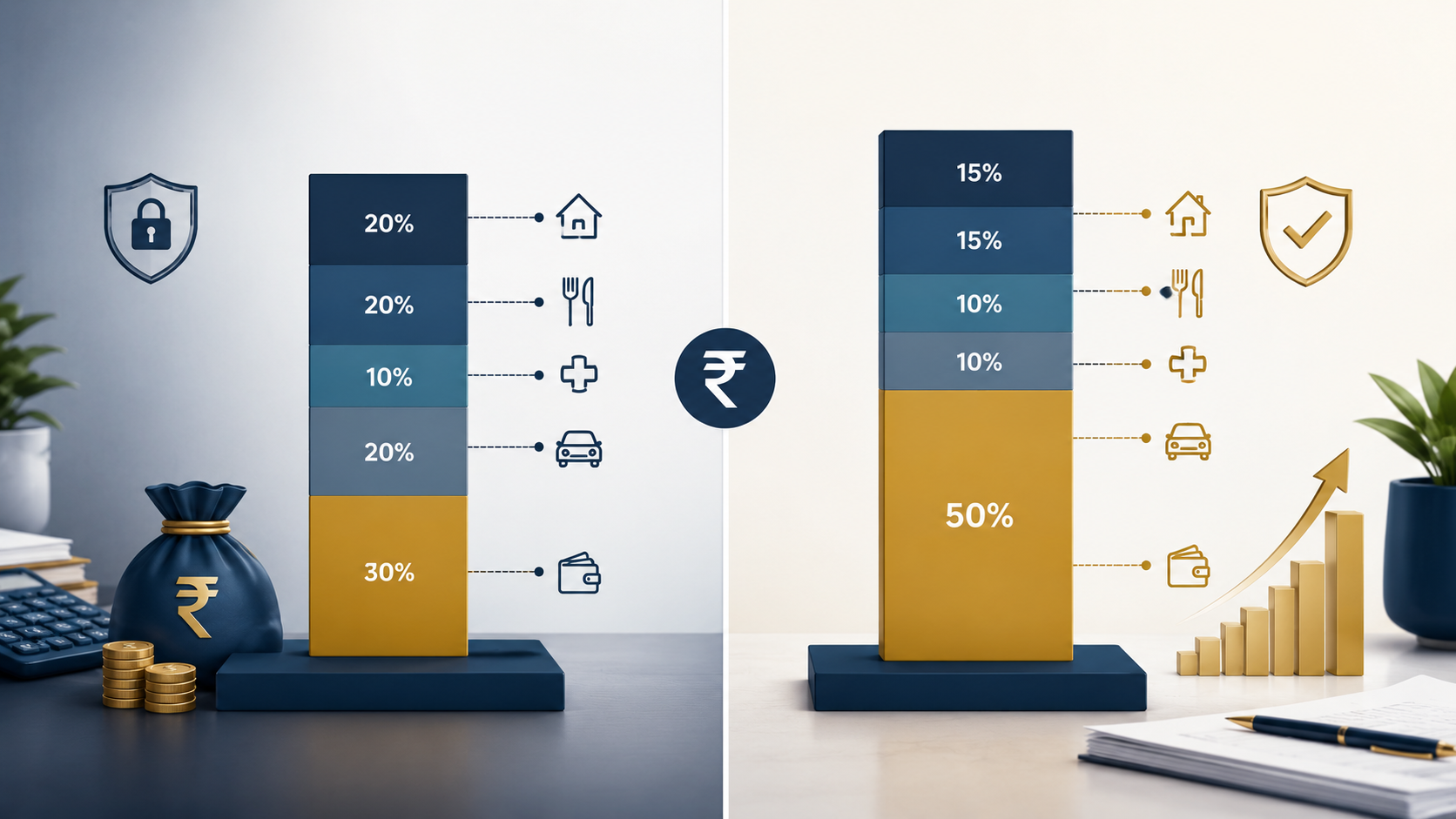

The 50% Basic Pay Rule Is Now Live — Has Your CTC Structure Caught Up?

The Rule Most Companies Are Still Ignoring The Code on Wages defines “wages” as at least 50% of an employee’s total remuneration. This means basic pay plus dearness allowance must constitute at least half of the Cost to Company. Allowances — HRA, conveyance, special allowance,…

-

Understanding Indian Laws Made Easy

Understanding Indian Laws Made Easy Understanding Indian Labour Laws Made Easy: A Simple Guide Introduction Expanding into the Indian market? Great move! With its booming economy and immense potential, India offers businesses incredible opportunities. However—and it’s a big however—compliance with Indian labour laws can feel…

-

Common Challenges in Statutory Compliance and How to Overcome Them

Common Challenges in Statutory Compliance and How to Overcome Them Common Challenges in Statutory Compliance and How to Overcome Them Introduction Statutory compliance is like the lifeline of every business—essential yet intricate. Whether you’re a startup or an established corporation, navigating the maze of Indian…

-

A Comprehensive Guide to Provident Fund (PF) Compliance

A Comprehensive Guide to Provident Fund (PF) Compliance A Comprehensive Guide to Provident Fund (PF) Compliance Introduction When it comes to statutory compliance in India, Provident Fund (PF) compliance is a cornerstone. Whether you’re running a small startup or managing a large enterprise, ensuring compliance…

-

Employee State Insurance (ESIC): What Employers Need to Know

Employee State Insurance (ESIC): What Employers Need to Know Employee State Insurance (ESIC): What Employers Need to Know Introduction Employee welfare isn’t just a nice-to-have—it’s a legal necessity. In India, Employee State Insurance (ESIC) is one such critical welfare scheme that provides medical, financial, and…

-

Professional Tax Compliance: A State-by-State Guide

Professional Tax Compliance: A State-by-State Guide Professional Tax Compliance: A State-by-State Guide Introduction When it comes to managing payroll and employee-related taxes, Professional Tax (PT) is an important compliance requirement for businesses in India. While the term “professional tax” might sound intimidating, it’s essentially a…

-

Labour Welfare Fund: Contributions and Compliance Explained (2026)

Labour Welfare Fund: Contributions and Compliance Explained (2026) Labour Welfare Fund: Contributions and Compliance Explained (2024) Introduction As of 2024, Labour Welfare Fund (LWF) continues to play a significant role in improving employee welfare in India. This statutory contribution ensures funding for initiatives like housing,…